by Tori Richie

Editor’s Note: Contributors to this post include Brian Esser, Principal, Sg2, and Trevor DaRin, Associate Principal, Sg2

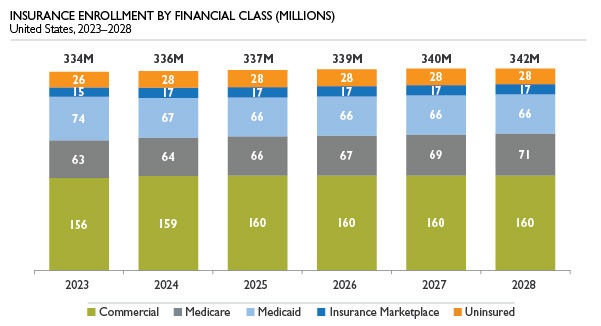

Each year Sg2 debuts the latest enrollment projections from our five-year Insurance Coverage Estimates (ICE) demand forecast. The team considers ZIP code level, age, federal poverty level, ethnicity and gender data to meaningfully distribute the population across financial groups. The following national trends were key inputs to the 2023 ICE model.

Note: Numbers may not add due to rounding. Sources: Sg2 Insurance Coverage Estimates, 2023; Claritas Demographics, 2023; Sg2 Analysis, 2022.

Unwinding the Public Health Emergency

For years Sg2 has tracked the pace at which baby boomers are aging into Medicare, the rise of high-deductible health plans and Medicaid expansion. However, this year brought about a new forecasting challenge—the eventual unwinding of the public health emergency (PHE) declared amid the COVID-19 pandemic.

The Families First Coronavirus Response Act, enacted by Congress in March 2020, contains a continuous coverage requirement that prohibits states from disenrolling individuals on Medicaid for the duration of the PHE, regardless of eligibility status. As a result, Medicaid enrollment has boomed. At the time of this year’s refresh, the most recent Medicaid data available was the July 2022 enrollment report, which showed 26% growth in enrollment since February 2020. The question is twofold: where will individuals on the now-inflated Medicaid rolls go when the PHE expires, and do some enrollees already have alternative coverage and are thus being double counted?

Sg2 expects the PHE to end at some point in 2023, and considering Medicaid’s 14-month renewal period, declines in Medicaid enrollment are most likely to impact enrollment in 2024 and 2025. Following the expiration of the PHE, Kaiser Family Foundation estimates between 5 million and 14 million people will lose Medicaid coverage. Medicaid attrition will be two pronged: individuals who are no longer eligible and thus removed from the Medicaid rolls, and individuals who are part of the churn population (those who experience a temporary loss of coverage by disenrolling from and then reenrolling in Medicaid within a short time frame).

Some of those no longer eligible are likely currently enrolled in another form of insurance, and they’ll experience no gap in coverage. Others will be faced with the decision to enroll in another form of insurance or become uninsured. Sg2 anticipates substantial increases in Affordable Care Act marketplace enrollment, as navigators (and other mechanisms that are part of state-level initiatives) are in place to assist those rolling off Medicaid.

Sizing the churn population proved less straightforward. This group is eligible for Medicaid but may slip through the cracks. People experiencing language barriers, reduced access to broadband internet or changes in housing are among those most at risk of losing coverage. State Medicaid programs are working to mitigate this impact by implementing continuous eligibility, adopting CMS 1902(e)(14)(A) waivers, and improving accessibility of enrollment materials and outreach efforts. Though available information is limited, the impact of these programmatic enhancements is an area Sg2 continues to closely monitor for future forecast updates.

Providers can play an important role in helping this population navigate enrollment.

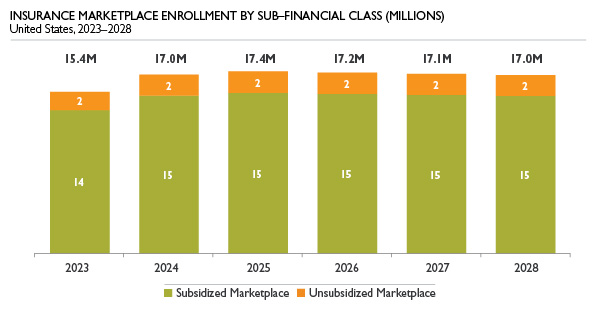

Growing Insurance Marketplace Enrollment

With record marketplace enrollment seen in 2022, Sg2 anticipates continued growth for 2023 and 2024. Subsidies introduced by the Biden administration have been extended through 2025 through the Inflation Reduction Act. The “family glitch” has been fixed in advance of open enrollment for 2023, which will improve plan affordability by considering the cost for a family to participate in an employer-sponsored health plan instead of the employee alone. This improvement will ultimately make more families eligible for exchange subsidies. In addition, navigators are funded to assist with enrollment for those who will lose Medicaid coverage once the PHE expires.

With the next presidential election in 2024, it is difficult to anticipate how funding for the exchanges may change for the 2026 open enrollment season and beyond. As such, Sg2 held marketplace forecast trends steady for 2026 through 2028.

Note: Numbers may not add due to rounding. Sources: Sg2 Insurance Coverage Estimates, 2023; Claritas Demographics, 2023; Sg2 Analysis, 2022.

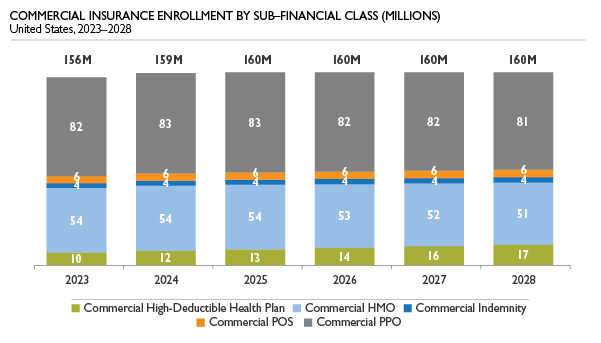

Rise of High-Deductible Health Plans

Modest increases in commercial coverage are expected as pressure mounts for employers to provide health coverage to employees. Despite efforts to offer more robust health care benefits, employers must contend with rising health care costs. Willis Towers Watson (WTW) found employers expect health care costs to rise 6% in 2023, and seven in 10 expect costs to rise over the next three years. As a result, Sg2 anticipates growth in high deductible health plans to continue over the next five years. Rising costs and ongoing cost shifting to employees will push employers to seek cost-effective care. Providers seeking to position themselves to capture lucrative commercial patients may consider direct-to-employer strategies focused on bundles, centers of excellence or total cost of care strategies.

Note: Numbers may not add due to rounding. HMO = health maintenance organization; POS = point of service; PPO = preferred provider organization. Sources: Sg2 Insurance Coverage Estimates, 2023; Claritas Demographics, 2023; Sg2 Analysis, 2022.

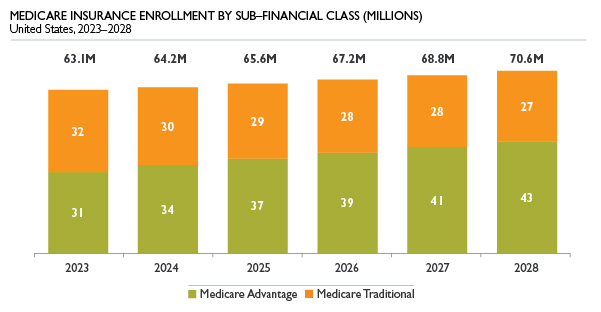

Raising the Ceiling on Medicare Advantage Penetration

Sg2 expects Medicare Advantage penetration to reach 50% in 2023, and growth will continue for the foreseeable future. No-cost premium plans have driven recent growth, and the economic environment means many consumers will continue to prioritize low-cost options. In this competitive space, payers are pouring more resources into Medicare Advantage marketing efforts, particularly in smaller markets, boosting enrollment. In addition, larger markets are exhibiting strong Medicare Advantage growth that does not appear to be slowing any time soon. Historically, 70% penetration was the rough saturation point for Medicare Advantage in legacy markets (California, Florida, Minnesota), but the appeal of supplemental benefits and $0 premiums is pushing that ceiling upward.

This trend has important downstream health care utilization impacts for providers. Increased adoption of Medicare Advantage has led to declines in potentially avoidable admissions, ED visits, skilled nursing facility visits and hospice care as payers better manage cost and quality for their patient populations. Increased adoption of Medicare Advantage also presents organizations with the opportunity to partner with payers and providers on shared savings arrangements.

Note: Numbers may not add due to rounding. Sources: Sg2 Insurance Coverage Estimates, 2023; Claritas Demographics, 2023; Sg2 Analysis, 2022.

Key Takeaways

Following nearly three years of operating in a pandemic environment under the PHE, Sg2 anticipates significant shifts in coverage in 2023 and beyond. The expected unwinding of the PHE will most directly impact Medicaid enrollment as states are able to evaluate eligibility and trim those deemed ineligible. Providers play an important role in identifying patients who are eligible for Medicaid and assisting them in the enrollment process so coverage is not fully lost. Indirectly, both insurance exchange and uninsured categories will be impacted by the PHE dynamic. Both are expected to grow as individuals shifting off Medicaid and unable to secure employer-sponsored coverage flow into both categories. Lastly, inflation dynamics and fear of recession will drive consumers in both Medicare and commercial categories toward lower-cost health insurance options via Medicare Advantage and high-deductible health plans. Providers should be prepared for shifts in utilization patterns and recognize price sensitivity across categories over the next several years.

How to Learn More

To learn more about the methodology behind the forecast, listen to our 2023 Insurance Coverage Estimates podcast.

Sources: Medicaid.gov. Monthly Medicaid & CHIP application, eligibility determination, and enrollment reports & data. CMS. Accessed December 2022; Williams E et al. Fiscal and enrollment implications of Medicaid continuous coverage requirement during and after the PHE ends. Kaiser Family Foundation. May 10, 2022; Medicaid.gov. COVID-19 PHE unwinding section 1902(e)(14)(A) waiver approvals. Accessed December 2022; Wikle S. States must plan now to limit Medicaid churn when continuous coverage ends. Center for Law and Social Policy. July 2022; Norris L. IRS regulations fix the ACA’s ‘family glitch’ as of 2023. Healthinsurance. org. October 11, 2022; Norris L. Open enrollment for 2023 ACA coverage: what to expect. Healthinsurance.org. November 1, 2022; WTW. Employers move to stem rising healthcare costs and boost affordability [infographic]. November 2, 2022; Kaiser Family Foundation. 2022 Employer Health Benefits Survey. October 27, 2022; Sg2 Analysis, 2022.

- Share

Tags: commercial coverage, insurance enrollment, Medicaid, Medicare, Medicare Advantage, PHE, public health emergency